According to the International Council on Clean Transportation (ICCT), the U.S. and European electric truck markets are diverging sharply. Despite falling global battery costs, prices for Class 6–8 electric trucks in the U.S. have increased by 27% since 2020. In Europe, prices have dropped by 32% over the same period.

While European fleets benefit from declining costs and scale, U.S. fleets face inflated prices as a result of manufacturer pricing strategies and lack of investment in scaling electric truck production.

Here are three ways manufacturers are keeping fleets locked out of affordable electric trucks:

1. Manufacturing Costs are Artificially Inflated

While manufacturers often point to batteries and raw materials as the main cost drivers, recent analysis highlights a different issue. It found that non-component costs–such as assembly, capital investment, and overhead–are roughly double those of comparable diesel trucks.

Given the structural similarities between electric and internal combustion vehicles, this raises questions about whether manufacturers are embedding additional costs to recoup their research and development costs, rather than distributing these costs across their full product line.

Source: Upfront Pricing of eHGVs: Risks and Opportunities for Electric Truck Uptake, ERM

2. Favoring Shareholder Payouts over EV Investments

Legacy manufacturers have the capacity and financial strength to scale electric truck production, yet are prioritizing shareholder payouts over investing in zero-emissions technologies that would lower purchase prices for customers.

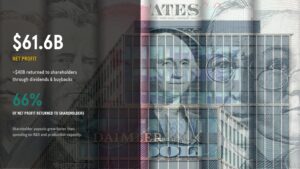

Between 2019 and 2024, five major European truck manufacturers generated ~$61.6 billion in net profit, returning roughly ~$40 billion–or 66%–to shareholders through dividends and buybacks. Over the same period, shareholder payouts grew faster than spending on R&D and production capacity.

This dynamic helps explain why investment in zero-emissions technologies has not kept pace with what is needed to drive costs down. While companies continue to invest, those investments remain modest relative to their revenues and financial capacity.

Source: Investments by European truck manufacturers into zero-emission technologies, Transport & Environment

3. A “Black Box” Pricing Culture

Because of the lack of price transparency within the trucking industry, it’s hard to know for certain what accounts for these high prices. This lack of pricing data has led states from California, to Colorado, Maryland, Massachusetts, New Jersey, New York, and Washington to take action to recommend or require pricing disclosures within state electric truck incentive programs in order to improve market transparency and empower fleet consumer choice.

New Competitors are Showing What’s Possible

New competition is beginning to reshape the electric truck market. Truck makers like Tesla are entering at scale, offering vehicles with longer range and significantly lower price points, resetting expectations for both performance and cost.

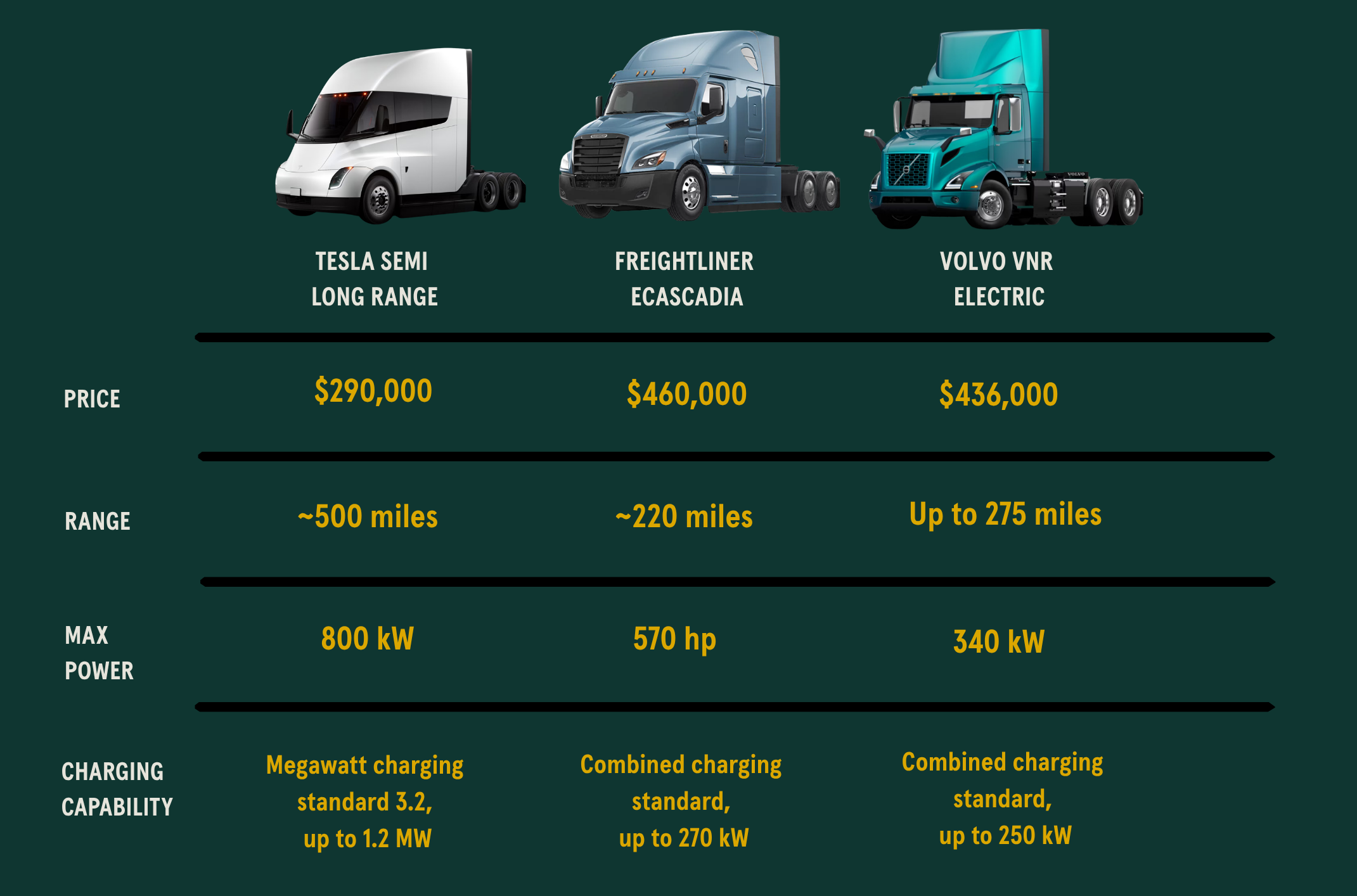

Now entering high-volume production, the Tesla Semi has a median price of around $290,000–that’s $170,000 cheaper than Daimler’s Freightliner eCascadia and with more than double the rang

Source: Truck electrification at a crossroads: How states can lead it in the right direction, ICCT

Data shows a growing preference among U.S. fleets for the Tesla Semi. In the past year, roughly 90% of applications in California’s electric truck incentive program have gone toward the Tesla Semi, a dramatic reversal from 2024, when 61% of funding supported trucks from legacy manufacturers like Daimler.

That momentum was on full display at this year’s ACT Expo in Las Vegas, where the Tesla Semi emerged as a focal point, highlighted by a Tesla customer’s announcement of one of the largest electric Class 8 truck deployments in California history.

As new competitors move to expand access and lower costs, many legacy truck manufacturers are moving backward instead of leaning into the demand signals that would accelerate that scale. This worrisome trend was a focal point at the annual general meetings of both Daimler Truck and Volvo Group.

The question then becomes what it will take for legacy manufacturers like Daimler and Volvo to support fleets in transitioning away from diesel and when they will start pricing their vehicles to remain competitive with new entrants like Tesla.